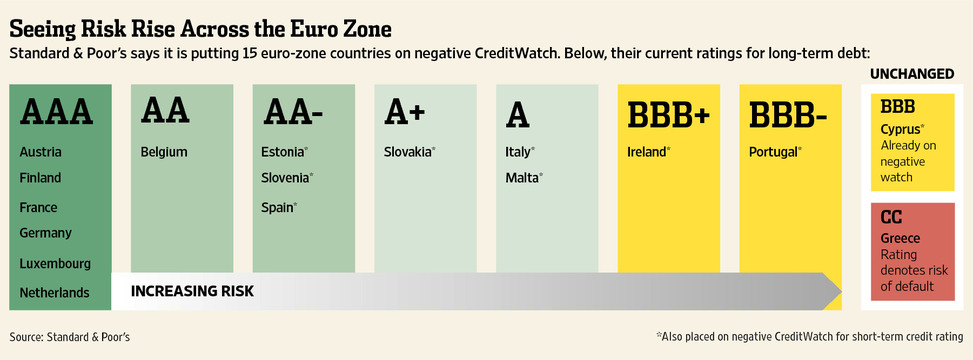

Markets were very volatile last week, featuring European Central bankers, the EU summit, potential credit rating downgrades, falling demand for eurozone government bonds and downward revisions of economic growth, all related to the on‐going sovereign debt crisis. After the downgrades of Belgium, Hungary and Portugal two weeks ago Standard and Poor did not beat around the bush. They placed 15 out of 17 of the eurozone bloc on watch for possible downgrade. On Friday, Moody's downgraded the three biggest French banks SocGen, Credit Agricole, and BNP Paribas by one notch. On global growth the IMF warned that it could lower estimates in January, just as the OECD did two weeks ago, lowering 2012 to 3.4% from earlier estimates of 4.6%, then 3.8%. The ECB, in cutting its interest rate to 1%, also cut its eurozone GDP growth for 2012 to 0.3% from 1.3% in September.

The attempts to solve the eurozone problems and save the common currency continue to struggle. Last week's summit ended up with 23 out of the 27 EU members agreeing to treaty changes, with three more ‐ Hungary, Sweden and the Czech Republic ‐ expected to join once their parliaments approve. Britain was left as the odd one out, but David Cameron had no choice after he was unable to persuade his EU colleagues to drop the Financial Transaction Tax that they believe is essential. Presumably we will now see financial firms moving to the UK, or Switzerland now that the tax is destined to be implemented just about everywhere else in Europe. The European Stability Mechanism ceiling will be 500 billion euros, but because of German opposition, the facility will not receive banking licence, and therefore will not be able to borrow from the ECB to lend to troubled EU states. However, the EU did manage to find an additional 200 billion euros from individual central banks to lend to the IMF for onward lending. Serious efforts are being made but the progress is slow and the markets do not seem to be convinced yet